Enforcement of Iowa ethics law is a joke.

Dubuque County Treasurer Eric Stierman and Winneshiek County Treasurer Wayne Walter stayed for free in a vendor’s Florida condo a few months ago, Ryan Foley reported for the Associated Press on March 13. The condo’s owner is Marc Carr, whose company GovTech Services collects local taxes for most of the state’s counties. The officials “denied any wrongdoing, describing Carr as a friend with whom they had previously vacationed in Florida.”

Iowa gift law does not exempt friends or vacations. While Stierman and Walter committed a particularly outrageous violation, their disregard for the code is hardly surprising.

For years, the Iowa State County Treasurer’s Association and the Iowa State Association of Counties have enabled and encouraged gifts to county treasurers from GovTech and SRI Incorporated, which handles online tax auctions. Since 2014, the two companies have paid for scholarships available only to children and grandchildren of county treasurers or their employees.

The mission of the association of counties is “to promote effective and responsible county government.” Yet the group’s top attorney Kristi Harshbarger helped devise a scheme to offer the scholarships despite the apparent gift law problem. Later, Harshbarger pushed back hard against an ethics board opinion that the program did not comply with the statute.

“A SHELL GAME THAT OBFUSCATES THE INTENT OF THE LAW”

Iowa Code Chapter 68B.22 states that public officials and employees, as well as their immediate family members, “shall not, directly or indirectly” solicit, accept, or receive gifts from a “restricted donor.” In addition, restricted donors “shall not, directly or indirectly, offer or make a gift” to public officials or employees. Restricted donors include anyone who “is or is seeking to be a party to any one or any combination of sales, purchases, leases, or contracts to, from, or with the agency in which the donee holds office or is employed.”

Vendors providing financial benefits to those wielding the power to extend their contracts is exactly the kind of arrangement the gift law is supposed to prevent. So when SRI and GovTech began offering four $500 scholarships to children or grandchildren of county treasurers or people working in their offices, Floyd County Treasurer Frank Rottinghaus was troubled.

Rottinghaus wrote to Harshbarger in November 2014 after the treasurer’s association announced the first winners (daughters of the Louisa, Mills, and Guthrie treasurers and the Appanoose treasurer’s grandson).

I’m concerned that the donation of $2,000 by SRI and GovTech Services is a clear violation of the Iowa gift law or at the least presents the appearance of an affront to the spirit of that law. I can see that this situation could be an embarrassment to the Treasurers Assn., ISAC [Iowa State Association of Counties] and all local elected officials.

“I am aware of this scholarship and I think it complies with Iowa’s gift law,” the general counsel for the counties wrote back. Harshbarger noted that “the vendors made the donation for the scholarships to ISAC’s Scholarship Foundation, which is a 501(c)(3) entity” and not a restricted donor. Also, a committee of treasurers selected the winners.

When we were approached about this scholarship for children of Iowa treasurers with a donation from vendors, we checked with Megan Tooker, executive director of the Iowa Ethics and Campaign Disclosure Board, on the legality of the situation. She said that the vendors could donate the money and the Foundation could give the scholarship, so long as the vendor didn’t select the recipient.

Rottinghaus then shared his concerns with State Representative Todd Prichard, who represents his area in the Iowa House. “I am surprised that the executive director of the IECDB would arrive at this type of interpretation. Appears to be a shell game that obfuscates the intent of the law to me.”

What Harshberger told Rottinghaus was accurate, but she didn’t mention that Tooker initially reached a different conclusion. Jones County Treasurer Amy Picray, then president of the treasurer’s association, reached out to the ethics board’s executive director in January 2014 to see if there was a gift law problem with “two vendors that would like to offer scholarships to graduating high school seniors who have a parent that work in a County Treasurer’s office.” (This exchange and other relevant correspondence are enclosed below as appendix 2.)

Tooker replied that a scholarship funded by a vendor “would be considered a gift.” A dependent child could not accept it if the “parent had to work for the government for the child to be eligible for the scholarship.” She told Picray that if any Iowa high school senior could apply, the program would fall under an exception to the gift law.

The general counsel for the association of counties proposed a different workaround. After consulting with a colleague, Harshbarger suggested that GovTech and SRI could donate to the county association’s scholarship foundation–“(and it’s tax deductible because the foundation is a 501(c)(3)).” The foundation could designate the funds “for the child of a treasurer,” and “The treasurers affiliate could select the recipients.”

You read that right. The ethics regulator stated the obvious: Iowa law does not permit vendors to give $500 to immediate family members of officials who keep their companies profitable. Instead of taking no for an answer, the attorney whose job is advising counties looked for a loophole to make this illegal gift possible–with a tax deduction for the vendors.

Apparently forgetting that the code says officials “shall not, directly or indirectly,” accept gifts from restricted donors, Tooker responded to Picray in February 2014, “I think this would work as long as the vendor doesn’t select the recipient. In other words, the vendor cannot reward someone for making purchases on behalf of the county.”

THE “PROGRAM VIOLATES IOWA’S GIFT LAW”

Prichard asked the Iowa Ethics and Campaign Disclosure Board for an advisory opinion on the matter. In August 2015, board members unanimously adopted a draft Tooker prepared (enclosed in full below as appendix 1).

The board found “the Iowa State County Treasurers’ Association’s scholarship program violates Iowa’s gift law because it is funded by restricted donors, the eligible recipients include immediate family members of treasurers and their employees, and the scholarship program is not available to the general public.” Key passage (emphasis added):

It is undisputed that a scholarship is a gift because the recipient does not provide anything of value in return for the grant-in-aid. The more difficult issue in this case is determining the donor of the gift. We believe the vendors that fund the scholarships are the donors. While the money provided by the vendors is first deposited in a third party’s bank account (the Iowa State Association of Counties’ scholarship foundation), and the recipients are selected by a committee instead of the vendors, we do not believe these factors change the ultimate source of that money. We are mindful that the gift law restricts gifts that come “directly or indirectly” from a restricted donor.6 We find these scholarships to be indirect gifts from the vendors that fund them. These vendors are restricted donors because they are either doing business or seeking to do business with county treasurers across Iowa and are financially impacted by whether a treasurer chooses to contract for their services.7 […] None of the exceptions in the gift law allows government employees or officials or their immediate family members to accept a scholarship from a restricted donor when the scholarship is not available to the general public. We note the effect of our decision would not be different if we had found the Iowa State Treasurers’ Association or the Iowa State Association of Counties is the donor of the scholarships because both of these entities are restricted donors due to the fact the counties pay dues to those organizations.

The opinion presented three ways to bring the program into compliance:

Tooker neglected to send the advisory opinion to the treasurers’ group or to the association of counties. In January 2016, the vice president of SRI e-mailed county treasurers inviting applications for four $500 scholarships, funded by his company and GovTech. Rottinghaus replied to Marshall County Treasurer Jarret Heil that he was “extremely surprised to have received this message” in light of the ethics board’s determination. “It is my expectation that you will be withdrawing this offer immediately.”

That’s what should have happened. The top lawyer for Iowa counties had other ideas.

“WE WOULD LIKE YOUR BOARD [TO] RECONSIDER”

Heil sought guidance from Harshbarger, who hadn’t seen the advisory opinion. After reviewing it, she wrote a sharp message to Tooker. She and the county treasurers were relying on Tooker’s February 2014 e-mail indicating “our process was compliant with the gift law,” Harshbarger noted.

If your Board was reconsidering this issue I would think the proper procedure would have been to notify the affected parties (ISAC, the Treasurer’s Association, and SRT/GTS) and allow us to be at the table for a discussion and opportunity to present our rationale under the law and the facts regarding the arrangement. […]

We would like your Board [to] reconsider this matter. I think their conclusion that restricted donor money retains its “restricted donor status” even after being given to an entity that is not a restricted donor is an erroneous conclusion under the law.

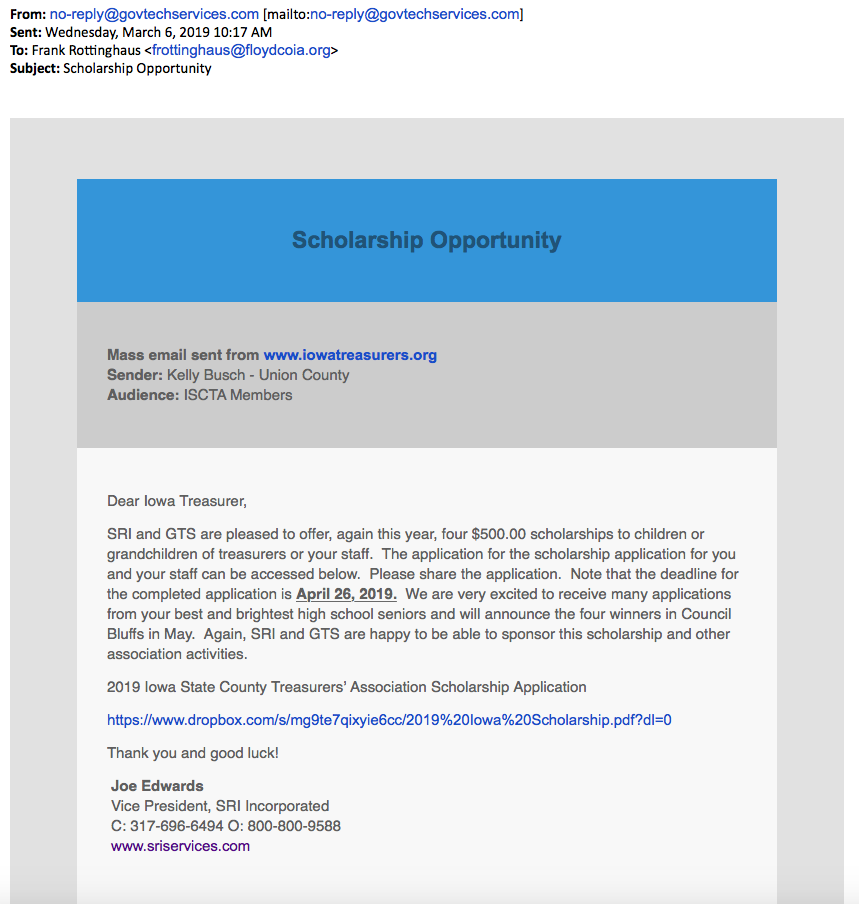

Give me a break. Every year, the vendors have proudly announced that they are funding the scholarships. Just last week, county treasurers received another call for applications from SRI’s vice president.

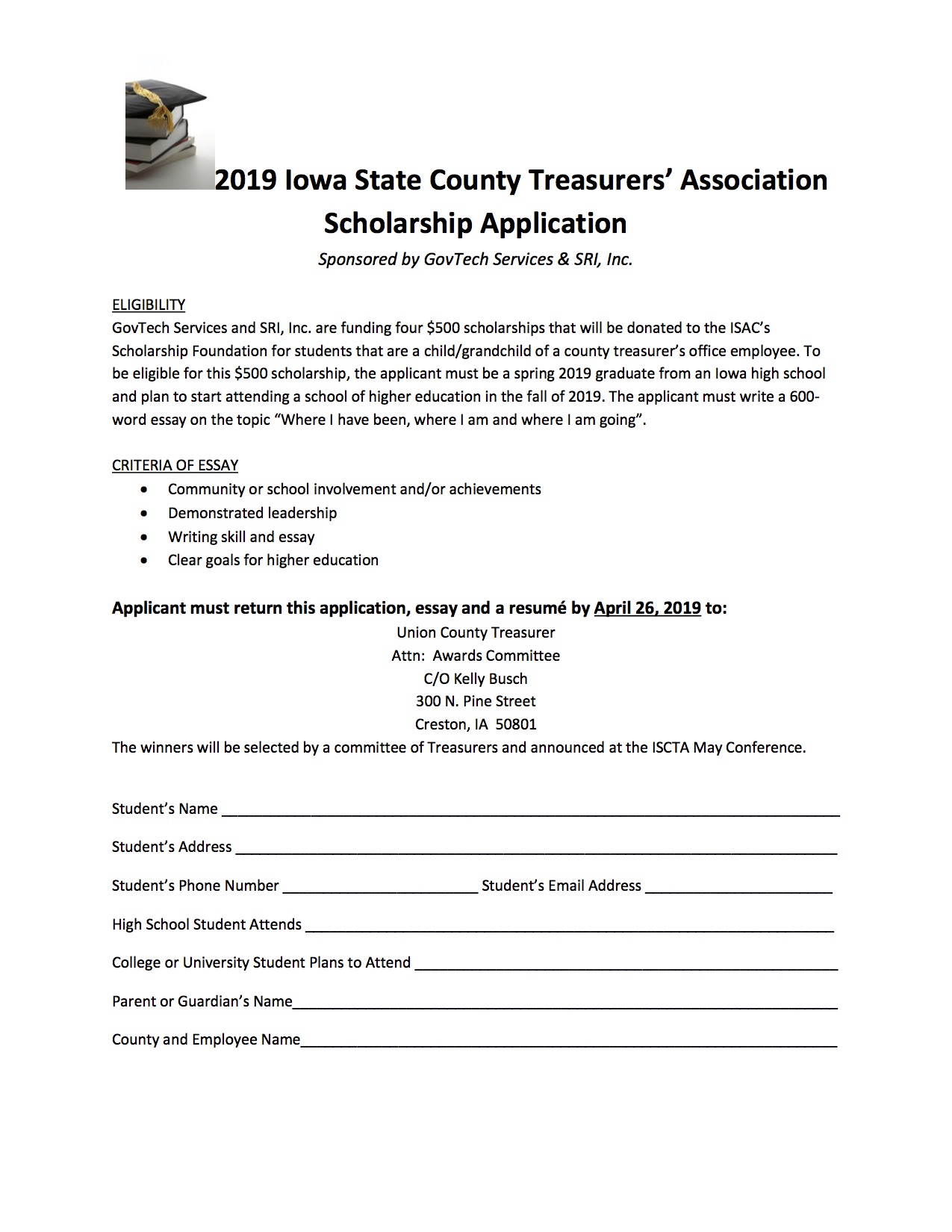

The latest scholarship application likewise states explicitly, “GovTech Services and SRI, Inc. are funding four $500 scholarships that will be donated to the ISAC’s Scholarship Foundation for students that [sic] are a child/grandchild of a county treasurer’s office employee.”

Harshbarger told GovTech’s owner Carr that she disagreed with the ethics board’s conclusion and would soon “discuss the going-forward plan” with ISAC’s executive director Bill Peterson. She later asked for a meeting with Tooker and the ethics board’s longtime chair, James Albert. Due to difficulties coordinating three people’s schedules, Tooker and Harshbarger met in March 2016 to “brainstorm possible options/alternatives to the scholarship.” Tooker wrote to her counterpart a few days later,

I talked to Jim [Albert] and he is very comfortable with how ISAC funds its scholarships [for children of county employees]. He likes that the scholarships are funded from many sources and that the vendors are getting something in return for their donation (ie. marketing exposure for sponsoring the golf outing). Thus, he thinks ISAC’s scholarship complies with section 68B.22 and I agree with you that probably the best thing for the treasurers’ association is to mimic as closely as possible how ISAC funds its scholarships.

Harshbarger told Tooker she would relay the information “to the treasurers’ association and will work with them to make the necessary changes.”

Remember, the ethics board had said the scholarship could be compliant if “solely funded by one or more non-restricted donors.” Now the board chair and executive director were saying the program could be “funded from many sources.”

“IN HINDSIGHT, I DON’T THINK WE SHOULD HAVE ISSUED THE OPINION”

When I inquired about the county treasurer scholarships in October 2018, Tooker backpedaled further, telling me (emphasis in original),

The Ethics Board does not have the authority to investigate or enforce complaints alleging local officials or employees are violating chapter 68B. See Iowa Code s 68B.32 (limiting our 68B jurisdiction to the executive branch of state government). Those complaints are to be filed with the county attorney. See Iowa Code s 68B.34A. The Board does have the authority to issue advisory opinions to local officials and employees concerning chapter 68B. Iowa Code section 68B.32A sets out the duties of the Board. It states the Board has the authority to:

12. Establish a procedure for requesting and issuing board advisory opinions to persons subject to the authority of the board under this chapter, chapter 68A, or section 8.7. Local officials and local employees may also seek an advisory opinion concerning the application of the applicable provisions of this chapter. Advice contained in board advisory opinions shall, if followed, constitute a defense to a complaint alleging a violation of this chapter, chapter 68A, section 8.7, or rules of the board that is based on the same facts and circumstances.

In 2015, Representative Prichard requested an advisory opinion on this topic. The subsection above allows local officials and employees to seek an opinion concerning chapter 68B, not the public at large. In hindsight, I don’t think we should have issued the opinion to Representative Prichard because he is not a local official or employee. As you can see from the chain of emails, I did a horrible job of informing the Association of the advisory opinion. If I had to do it over again, I would tell Representative Prichard that he could either file a complaint with a county attorney or he could encourage the Association to request an advisory opinion. Advisory opinions, in my opinion, are meant to ask permission for a proposed course of conduct rather than a means to prove a violation. I’m to blame for how we handled Representative Prichard’s advisory opinion request. I’m going to follow up with Association and see whether they would like to request an advisory opinion on behalf of their members, which are local officials and employees.

Tooker is hung up on the wrong mistakes. If Prichard wasn’t entitled to seek guidance about conduct by county officials, Rottinghaus could have done so in his capacity as Floyd County treasurer.

Ideally, Tooker would have invited all stakeholders to provide input and make their case to the ethics board in the summer of 2015. But a better process should have yielded the same result.

The problem wasn’t the advisory opinion, it was Tooker previously giving her blessing to a plan that in effect laundered vendors’ money through the association of counties. Everyone involved knew corporations profiting from relationships with treasurers were funding the gifts, and the only eligible beneficiaries were family members of those officials and their employees. Tooker and Albert should have stood their ground and defended the board’s conclusions, rather than bending over backwards to help Harshbarger and the treasurers keep the scholarships going.

“MY UNDERSTANDING IS THAT THEY DIVERSIFIED THEIR DONORS”

Harshbarger told me last October,

The conclusion that was reached by Megan in consultation with the IECDB Chair was that the funding for the scholarship should be diversified to either add additional sources other than just vendors (individual treasurers, etc) and/or to have the vendors get something in return for their donation (such as marketing exposure for sponsoring a scholarship fundraising event). I passed this guidance onto the treasurers’ affiliate.

Yet county treasurers did not change the program in any meaningful way. The mass e-mail from SRI’s vice president in April 2018 contained the same wording that appeared on this year’s call for applications: “GTS and SRI are pleased to offer, again this year, four $500.00 scholarships to children or grandchildren of treasurers or your staff. […] Again, GTS and SRI are happy to be able to sponsor this scholarship and other association activities.”

Many attorneys advise clients to avoid even the appearance of a conflict of interest. In this case, vendors continued to provide much (if not all) of the funding for the scholarships. The gift law forbids corporations from offering financial benefits in order to secure or preserve business relationships with public officials.

Last fall, Harshbarger ignored follow-up questions about why her organization would not strongly discourage treasurers from participating in the program.

After Foley reported on the two treasurers’ Florida adventure, I circled back, asking,

In retrospect, wouldn’t it have been wiser for ISAC to encourage strict compliance with Iowa gift law and avoidance of even the appearance of a conflict with respect to scholarships funded by vendors of the county treasurers?

It seems that ISAC’s willingness to be a party to this questionable scholarship program has emboldened some county treasurers to commit even more flagrant violations of the gift law. How would you respond to that critique?

Harshbarger replied on March 14,

ISAC of course encourages all of its members to strictly comply with Iowa’s gift law. ISAC does not, however, have any oversight or enforcement authority over the county officials in Iowa. We do our best to be an educational resource to Iowa’s county officials and employees on a plethora of topics that counties face. […]

As far as the treasurers’ association scholarships, I believe we have previously discussed the conflicting information the treasurers’ association received from IECDB on the matter. The most recent advice from IECDB was that the funding for the scholarship should be diversified to either add additional sources other than just vendors (individual treasurers, etc) and/or to have the vendors get something in return for their donation (such as marketing exposure for sponsoring a scholarship fundraising event). ISAC passed this guidance onto the treasurers’ association and encouraged them to make those changes.

The scholarships look like the same illegal gifts to me. Which part of Tooker’s advice did the treasurers implement, in Harshbarger’s view? “My understanding is that they diversified their donors. Again, I would encourage you to discuss the structure of the scholarship with the treasurers association.”

Jones County Treasurer Picray told me by phone on March 14 that the treasurers designated proceeds from an annual silent auction to the scholarship fund. Marshall County Treasurer Heil later confirmed via e-mail,

I was on the Treasurers executive board when the ethics board brought this to our attention. We spoke with legal counsel Kristi Harshbarger at ISAC about this. Based on her opinion and her discussion with ethics board we were advised to revise the scholarship to include additional private donations so it was not a scholarship funded only by vendors, which we implemented. The additional funds are from a fundraiser silent auction at our Treasurer’s conference. This additional funds through the silent auction was approved as compliant from legal counsel and their discussion with ethics board.

Additionally as advised, we implemented a policy that a panel of Treasurers select the scholarship winner, with no vendors on this panel.

A token amount of auction money does not change the reality that GovTech and SRI, by their own admission, are the main backers of four $500 scholarships a year. Tooker told Harshbarger in 2016 that Albert was comfortable with a program similar to ISAC’s other scholarships, funded by many sources.

The treasurers seem to have the gotten the impression from Harshbarger that their relatives can keep accepting gifts from vendors as long as the scholarship isn’t solely funded by restricted donors.

As mentioned above, the ethics board’s unanimous opinion in 2015 was that to be compliant, a scholarship program would have to be “solely funded by one or more non-restricted donors.”

Foley reported on March 14 that the future of the program is in doubt.

Iowa county treasurers said Thursday that they are reviewing whether to continue a college scholarship program funded by two key vendors that benefits their own children and grandchildren. […]

The Iowa State Association of Counties will discuss the program with the treasurers’ association, which is one of its affiliates, said executive director Bill Peterson. He said his group, which administers the scholarships, wants to ensure that changes it recommended after the 2015 ethics board opinion were implemented by the treasurers.

“If we’re unsatisfied, I would say that we would refuse to assist them further with the administrative details of how they handle their scholarship funds,” he said.

Peterson didn’t answer my follow-up questions. His watchdog act is not convincing. Every step of the way, ISAC’s general counsel has facilitated this program: getting initial approval to funnel money from vendors through her organization, vigorously defending the arrangement after the setback with the ethics board, and reassuring treasurers that any small gesture to “diversify” could keep funds flowing from restricted donors.

Incidentally, Harshbarger told me the Dubuque and Winneshiek treasurers were consulting with the ethics board and “are also working with their county attorneys and will take steps as possible to rectify any unintentional violations of Iowa’s gift law.” If longtime county officials weren’t aware it was illegal to accept free lodging from a vendor, that reflects poorly on ISAC’s work as an “educational resource.”

Tooker confirmed,

Mr. Stierman and Mr. Walter have been in touch with me. I advised them to contact their respective county attorneys to discuss what they need to do to comply with the gift law. Mr. Stierman said he would also like an advisory opinion from the board. I told him he should put in writing how he plans to ensure compliance with the gift law in the future with respect to the restricted donor’s condo or similar matters. The Board can then issue an advisory opinion stating whether the board members agree his proposed course of action would comply with the gift law.

Final note: In January 2016, Harshbarger submitted an amicus curiae brief on ISAC’s behalf to the Iowa Supreme Court. The brief argued that almost all Iowans with felony convictions should be barred from voting for life, because changing the system would be too inconvenient for county auditors. The very same week, Harshbarger was arguing with Tooker and looking for angles to salvage the treasurer scholarship program.

Here’s an idea for the counties’ general counsel: stay in your lane and focus on keeping your own constituency from committing crimes.

P.S.–GovTech removed video testimonials from Stierman and Picray from its website on March 14 (AP grabbed a screen shot in time). As of March 15, a written testimonial from Picray remains on the company’s front page.

Appendix 1: August 2015 advisory opinion from Iowa Ethics and Campaign Disclosure Board

Appendix 2: E-mail correspondence and other records related to the ethics board’s consideration of the county treasurer scholarship program (many documents in this file are duplicates)

Appendix 3: December 2014 e-mail correspondence among Floyd County Treasurer Frank Rottinghaus, Iowa State Association of Counties legal counsel Kristi Harshbarger, and State Representative Todd Prichard